On September 9th, 2020 the Finance Minister Smt Nirmala Seetharaman released the Performance of PSB on EASE 2.0 Index ranking covering the period March 2018-2020. In the said release FM said Financial Services will be a part of the Doorstep Banking Services available to PSB Customers from October 2020 onward. This move was expected to particularly benefit Senior Citizen and Divyang. Currently only Non-Financial Services such as pick-up of cheques and Demand Drafts was available through Doorstep Banking Agents.

- It was launched in January 2018 jointly by the government and PSBs.

- It was commissioned through Indian Banks’ Association and authored by Boston Consulting Group.

- EASE

Agenda is aimed at institutionalizing CLEAN and SMART banking.

- The Index measures performance of each PSB on 120+ objective metrics

EASE 2.0 builds on the

foundation of EASE 1.0 and introduces new reform Action Points across six

themes to make reforms journey irreversible, strengthen processes and systems,

and drive outcomes.

The six themes of EASE

are:

- Responsible Banking.

- Customer Responsiveness.

- Credit Off-take.

- PSBs as UdyamiMitra (SIDBI portal

for credit management of MSMEs).

- Financial Inclusion &

Digitalisation.

- Governance and HR.

EASE Reforms Index:

The Index measures performance of each PSB on 120+ objective metrics.

The Index follows a fully transparent scoring methodology, which enables banks to identify their strengths as well as areas for improvement.

The goal is to continue driving change by encouraging healthy competition among PSBs.

Bank of Baroda, State Bank of India, and erstwhile Oriental Bank of Commerce were felicitated for being the top three (in that order) in the ‘Top Performing Banks’ category according to the EASE 2.0 Index Results.Bank of Maharashtra, Central Bank of India & erstwhile Corporation Bank were awarded in the ‘Top Improvers’ category basis EASE 2.0 Index.

Punjab National Bank, Union Bank of India, and Canara Bank were also recognized for outstanding performance in select themes.

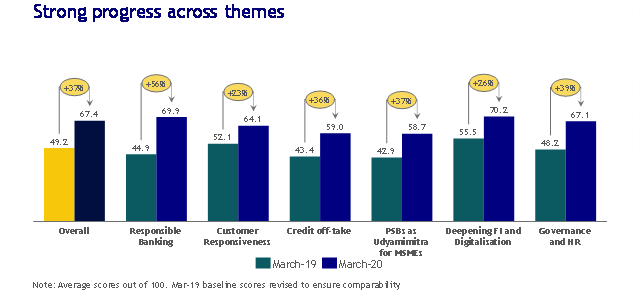

PSBs have shown a healthy trajectory in their performance over four quarters since the launch of EASE 2.0 Reforms Agenda. The overall score of PSBs increased by 37% between March-2019 and March-2020, with the average EASE index score improving from 49.2 to 67.4 out of 100. Significant progress is seen across six themes of the Reforms Agenda, with the highest improvement seen in the themes of‘Responsible Banking’, ‘Governance and HR’, ‘PSBs as Udyamimitra for MSMEs’, and ‘Credit off-take’.

PSBs have adopted tech-enabled, smart banking in all areas, setting up retail and MSME Loan Management Systems for reduced loan turnaround time and PSBloansin59 minutes. comand, TReDS for digital lending. PSBs have instituted real-time visibility to retail and MSME customers on the status of their loans. Most branch-based services are now accessible from home and mobile, including in local languages.

EASE Reforms Index has equipped Boards and leadership for effective governance, instituted risk a appetite frameworks, created technology- and data-driven risk assessment and prudential underwriting a and pricing systems, introduced Early Warning Signals (EWS) systems and specialised monitoring for t ti me-bound action in respect of stress, put in place focussed recovery arrangements, and established outcome-centric HR systems.

Major Reform achievements between March 2018 to March 2020

- Most PSB customers now have access to 35+ services such as IMPS, NEFT, RTGS, intra-bank transfer, account statement, cheque book request on mobile/ Internet banking and23 services such as chequebook issuance, cheque status, issuance of form 16A, block/activate debit card on the call centre. The availability of services has nearly doubled over the last 24 months.

- Nearly 4cr active customers on mobile and internet banking with 140% increase in financial transactions through mobile and internet banking channels and almost 50% of financial transactions through digital channels.

- Call centers now offer services in 13regional languages such as Telugu, Marathi, Kannada, Tamil, Malayalam, Gujarati, Bengali, Odia.

- Complaint redressal average turnaround time reduced from the average of approximately 9 days to 5 days

- 23 branch-equivalent services such as account opening, cash deposit, cash withdrawal, fund transfer made available by PSBs through Bank Mitras

- PSBs have issued RuPay credit cards to nearly 23 crore basic savings account customers

- Significant improvement in customer outreach through dedicated marketing force and external partnerships. The number of dedicated marketing employees has increased from 8,920 to 18,053.

- Sourcing of retail and MSME loans through the dedicated sales force and marketing tie-ups has increased nearly five times from 1.5 lakhs to 8.3 lakh loans

- Turnaround time (weighted average) for retail loans reduced by 67% from the average of nearly 30 days to nearly 10 days

- Cross-sell of non-banking financial products has made available bouquet of financial products to the customer

- For prudential lending, PSBs are now systematically keeping watch on adherence to risk-based pricing, and cases with deviation have reduced from 59% to 20%, and have put in place data-driven risk-scoring for appraisal of high-value loans that factors in group-entities.

- Most PSBs have deployed IT-based EWS systems leveraging third-party data, which have enabled early, time-bound action in stressed accounts. Monitoring has also been strengthened by deploying Agencies for Specialised Monitoring, and proactively monitoring listed entities based on published financials. Slippage into NPA has reduced from 3.90 lakh crore in 12-months ending March-18 to 1.45 lakh crore in 11-months ending February-20.

- PSBs have adopted digital platforms such as online OTS, e-Bक्रय, e-DRT for expedited recovery. 88% of one-time settlement (OTS) cases are now tracked through dedicated IT systems.

- PSBs have adopted new ways of credit, such as PSBloansin59minutes.com and Trade Receivables Discounting System (TReDS) for digital lending for MSMEs and retail. 73% of all PSB inland bills are now discounted through online TReDS.

- The Government has introduced several governance reforms. The governance reforms include arm’s length selection of top bank management through Banks Board Bureau, introduction of non-executive chairpersons, broader talent pool for such selections, empowered bank Boards, strengthening of the Board committees system, enhancing the effectiveness of non-official directors, and leadership development and succession planning for the top two levels below the Board. In larger PSBs, Executive Director strength has been increased, and Boards are empowered to introduce CGM level for increased business.